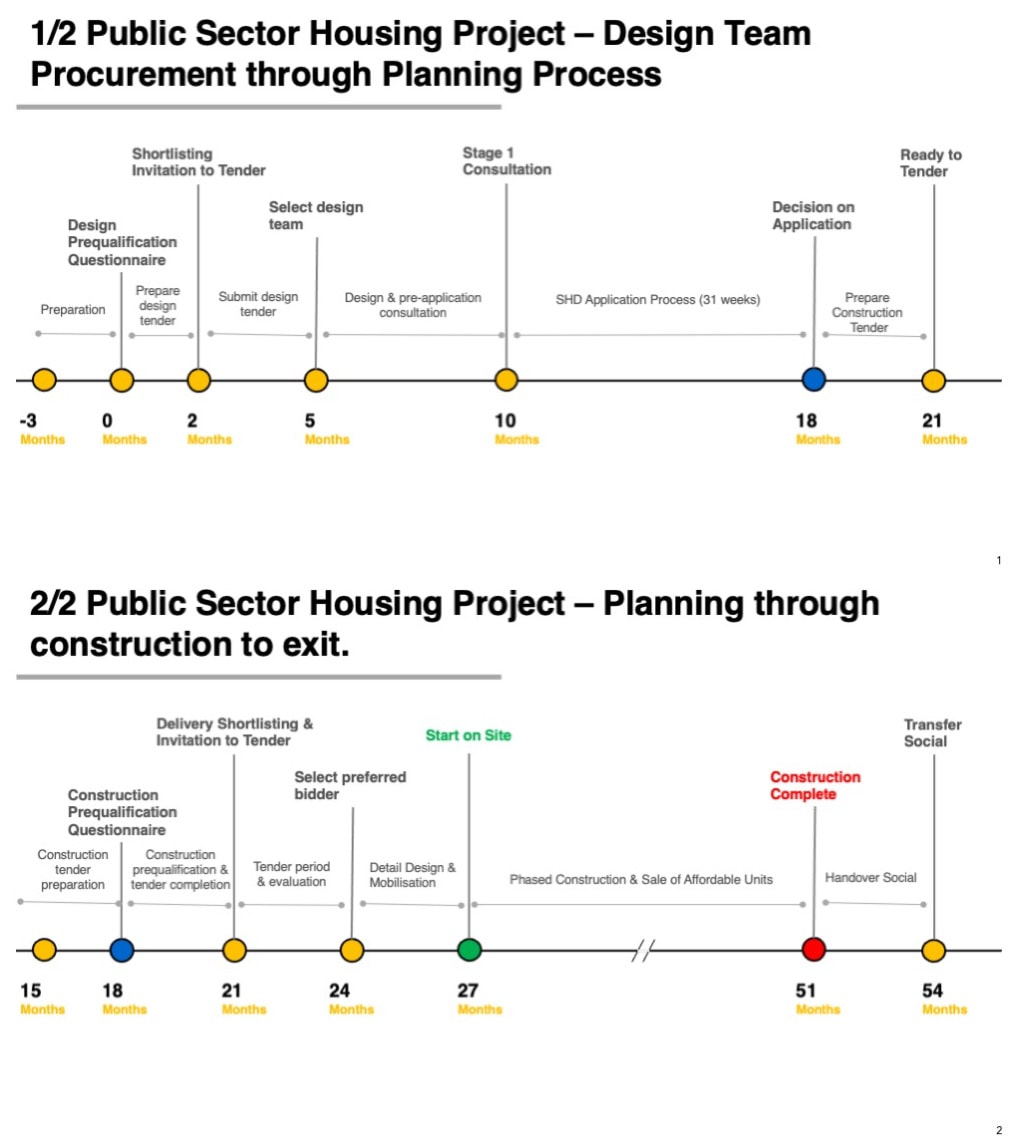

Delivery of housing at scale by the State is going to take time. What do we do in the meantime?21/5/2021  There is no doubt that a mix of #publicsector and #privatesector delivery of homes is going to be required to target delivery of 35,000 homes per year. There are a number of sequential steps and approvals that ensure public delivery gets value for the State's money and that the #procurement is open to as wide a range of providers as possible. The reality is that starting with site ownership and with a very efficient process it takes time - the public supply tap cannot be turned on and houses provided tomorrow. How the State provides homes in the interim period will require a number of approaches including #procurement of homes through lease and purchase from the market. A situation where local authorities, AHBs and other agencies are bidding against each other or individually negotiating and driving up prices does not get good value - this needs to be thought through.

A more detailed analysis of the comparison between the public and private approach is given in this post - www.keoconsult.com/knowledge/housing-procurement-delays-key-is-the-duration-of-the-project-governance-process-not-the-procurement-process

0 Comments

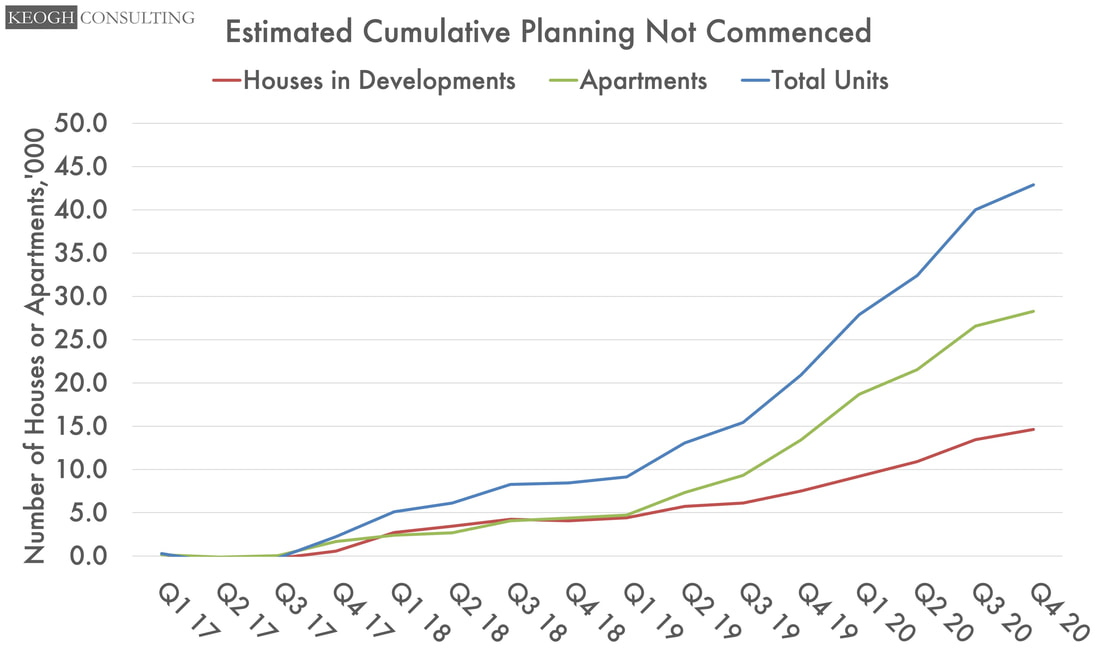

Trend in overhang of parked residential projects indicates ongoing viability issues for projects18/5/2021  Calculating from the CSO's latest figures the trend in planning permissions obtained but not commenced for apartment and multi housing development has been increasing for some time. In the face of demand exceeding supply by a significant factor the ongoing delay in projects starting can be attributed to viability issues, lack of funding or simply developers looking to sell on ready to go sites. Interventions that further impact on viability, reduce the level of funding in the market or increase the cost of ready to go sites are not going to get parked projects moving.

Impact on Required Sale Price to Cover Increase in Part V S&A to 20% With news that proposals are going to Cabinet in the coming weeks to mandate builders to provide 10% of new developments to local authorities as social homes, and a further 10% as affordable housing the impact will be to increase price of homes for private purchasers (as required return on a project would then have to be achieved from selling a smaller number of units for sale to private purchasers). The scale of impact will vary but for a typical standard 2 bed apartment in an SHD type development this could add €9.5k (+2%) to the required sale price (with the average cost for a LA to purchase a 2-bed unit in such a development being €360.4k). For a 3-bed house the required price will increase from €338k to €346k (+2.5%).

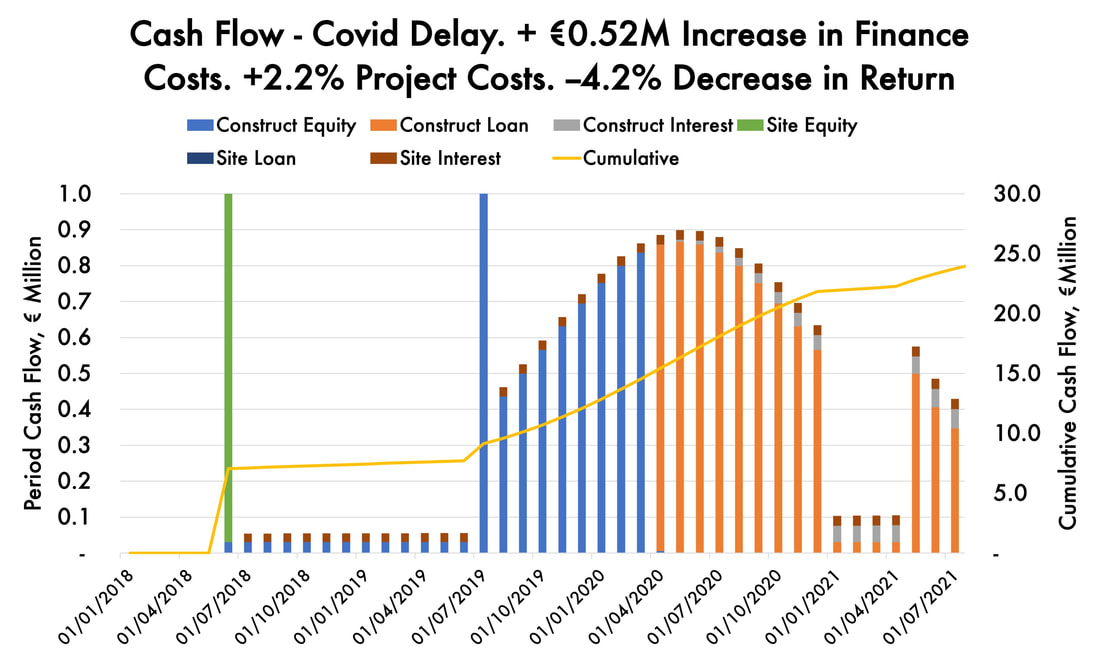

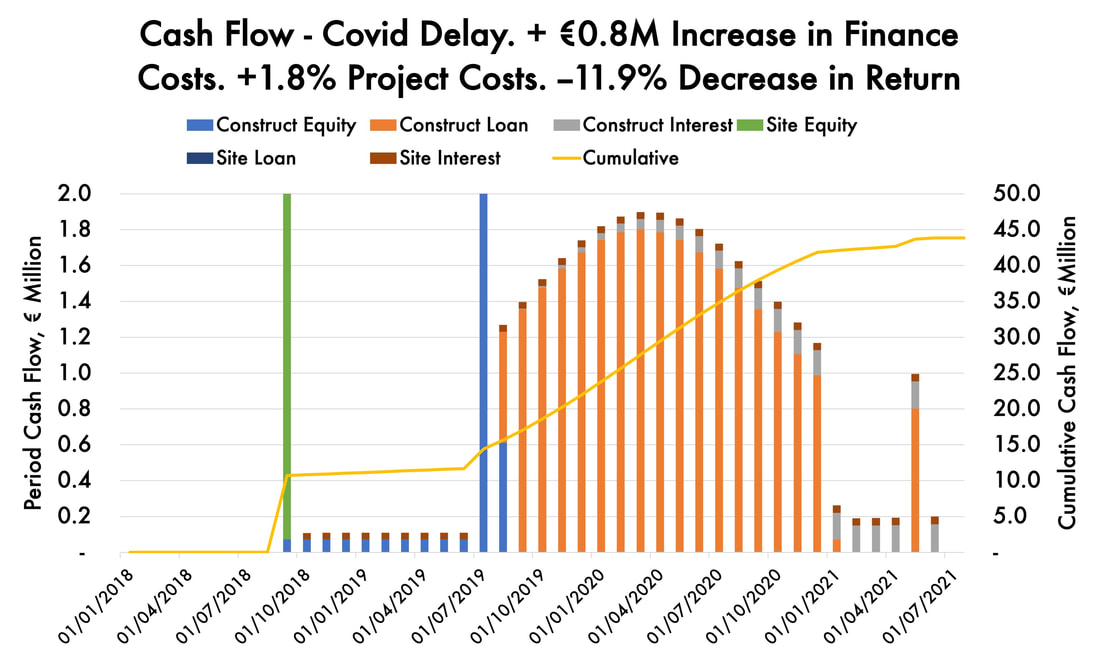

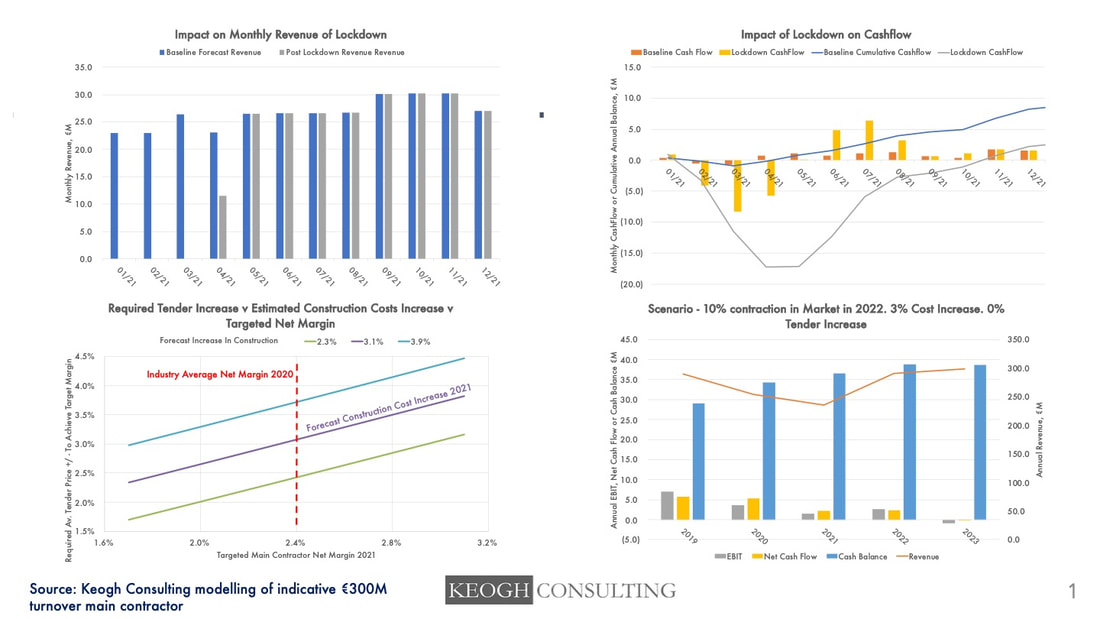

With residential development closed down since January (in addition to the 2020 lockdown) the financial hit is significant. To put in perspective - the delay to Oakmount Groups development of 48 apartments in Dublin may add up to €0.5M to their project costs. This is approximately equivalent to the revenue from one unit and adds over 2% to project costs.  Impact on 48 unit apartment development The picture is the same for commercial development with projects stalled and no return to site date in place. With such uncertainty around delivery date this impacts on a developers ability to get a tenant in place. Further delays will make a bad situation worse. The example below illustrates the impact on Valorem Investment Partners project on Newmarket Square, Dublin 8.  Impact on 9,400 sq m commercial development Dublin 8  Covid is having a huge impact on construction companies in Ireland - it is critical that construction activity commences again for the health of these companies. Our report looks at some of the issues facing builders and recommends a number of actions - download here

|

About Us

Keogh Consulting looks to help individuals and organisations deliver the right projects the right way. Here is some of our knowledge and a few case studies that we hope will help you on your project journey.

Categories

All

Project Cost Calculator & Database

Cost Rental Simple Model

Cost Rental Complex Model

|

RSS Feed

RSS Feed

Service |

Company

|

|