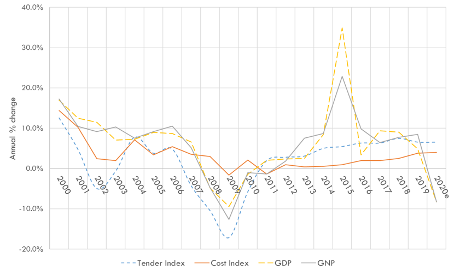

GDP, GNP, Construction Tender & Cost Trends Ireland is currently in the middle of the COVID-19 crisis with significant economic and health impact throughout the island. The Irish Government have looked to shield the economy and have put in place stay at home measures. Construction had been stopped in Ireland up to 18th May with sites starting to reopen last week. An economic contraction is forecast with the IMF[1] forecasting a contraction of -7.5% in real GDP in the Euro Area (v -4.5% in global financial crisis 2009) for 2020. The ESRI[2] have forecast a contraction of -7.1% in GDP with a 12 week shutdown. Hopefully this contraction may reverse when the stay at home policy is reversed on a phased basis, however, it is possible that it may take until early 2022 until GDP in Ireland recovers to current levels.

This crisis will a) shift the demand curve for housing (given reduced household incomes), b) reduce the supply of housing (given reduced housing output) and c) increase cost of delivery (given increase in programme related costs, reduced productivity and delay in sales and completions). This paper (download full paper here) looks at the impact of these changes. With the current housing supply deficit demand for housing will remain after the COVID-19 crisis with a mix of tenure types required in the market – however, the affordable price point for purchase will change, at least in the medium term, with viability of development issues given that pool of able purchasers may have shrunk. Housing demand - In 2020 & 2021 our forecasts indicate that there may be a change in overall demand due to migration changes on account of COVID-19. With no emigration or immigration due to global travel restrictions, we estimate a net migration decrease on account of these restrictions from 34k to c17k. This forecast indicates that overall demand for housing may fall to below 25,000 in 2020 & 2021 before rising again in 2022 to above 30,000 as hopefully migration flows resume. This demand will be made up of a range of tenure types. Housing supply – Covid-19 has halted construction activity in Ireland since the beginning of March. A phased restart of construction activities on sites has commenced since 18th May. Reduced completions will create further supply difficulties in the housing market and increase the housing supply deficit. We estimate the reduced construction output could increase housing supply deficit by 21k units in period to 2022. Construction Industry Economic Output - With the reduced number of completions a reduction in residential construction output of €4.6bn in 2020 & €3.8bn in 2021 is forecast – this will have significant impact on employment, GNP & exchequer returns. The exact impact on construction costs is unclear at present – the cost of site safety measures and programme extensions will have to be recovered of profitability will be impacted. Housing Prices – On account of the COVID-19 lockdown there have been little or no transactions in the market since early March[3]. The impact on home prices is unclear but will depend on a number of factors including speed of recovery, unemployment, average incomes and global economic trends including FDI landscape moving forward. This will make affordability more difficult with a lowering of the number of potential purchasers for new homes (with consequent increase in demand for other tenure types). Gross Household Incomes – Given current economic conditions it is likely that income levels will at best stay flat and in all lilklihood decrease through 2020. Banks probable unwillingness to advance loans to potential purchasers on reduced incomes on account of temporary COVID-19 measures will stop transactions, make affordability for potential purchasers (particularly those workers in high-contact sectors) more difficult and reduce demand for housing at current price levels. Impact on FTB Numbers – Our calculations indicate that at the economically viable house delivery price of €325k there may be potentially 12.5% less households able to purchase over pre Covid period (approximately 225k households may have fallen out of the affordability net[4]). Affordability – Based on uplifted CSO13 household income data adjusted for Covid-19 impact:

Could offsetting VAT payments for a purchaser help – Some commentators have suggested that payment of VAT over an extended period could help affordability. We have analysed such a scheme – implementation of such a scheme would lower the upfront cost of purchasing a home by transferring some of the risk from a funder to the State and allow a household with lower gross income purchase a home. However, it would increase the monthly housing cost for a household – the same impact could be achieved with an increase in LTI multiplier of 4.0x and result in a €180 per month saving over the cost of illustrated VAT offset scheme. Shared equity scheme – A specific and targeted state shared equity scheme could help lower barriers to home ownership for households and mitigate affordability challenges facilitating prospective buyers with average household incomes to get a foothold on the property ladder. Careful consideration would have to be given to the design of the scheme to ensure fairness, transparency, effectiveness and affordability while making sure that it takes account of Central Bank macro prudential rules. A household with a €60k income would save €3,080 per annum over annual average rental cost for a 2 bed townhouse with a combination of 30.4% shared equity loan and a standard mortgage for the remainder. Filling the Housing Supply Gap – With exchequer receipts generated on account of construction of an apartment estimated to amount to €134k per unit (house €99k per unit) – assuming a 130% shadow cost of government funding would imply that a stimulus programme costing up to €103k per apartment (house €76k per unit) would have a cost benefit ratio of 1. With full employment and a deficit of construction capacity such a measure may have had negligible stimulus impact up to now and perhaps resulted in price increases. However, given that the current crisis has reduced manning levels of construction sites and consequently employment, there may be spare construction capacity that could be put to use on opening sites that up to now were not viable but with a stimulus could become economically viable – getting homes that otherwise would not be built, built! Conclusion Housing developers need to have an understanding of prospective purchasers affordability levels and how the current crisis may have impacted their ability to purchase a new home. Now is a time to reappraise and stress test projects under differing scenarios regarding input costs and achievable price targets to determine their vulnerability. Priority should be given to those with highest risk adjusted returns and where possible these projects should be progressed through preliminary design, planning, procurement to get to a shovel ready state. This understanding of delivery costs, affordability levels of potential purchasers and number at each price point is key in prioritising projects and may allow more sites to open and excess construction capacity to be used to progress construction projects – this paper looks to examine these questions. Assuming demand for housing holds, albeit at a different price point, there will be an ongoing need for residential developers to contract with main contractors and a range of sub contractors in their supply chains in the future. Thus, while activity on sites is ramping up or paused, it is imperative to retain two way relationships between developers and their supply chain given current exposure to significant risks on all sides. Given new site measures that must be in place a focus should be made on improved workflow and coordination of activites on sites to minimise productivity reductions and indeed capture productivity opportunities. Collaboration is key and working together the future can be planned to minimise impact on profitability throughout the housing supply chain through formulating the most appropriate mitigation strategy for effective delivery,. Finally, given market failure to provide the number and mix of housing types required on account of economic viability issues, the State needs to consider the best way to provide stimulus to encourage construction of houses and ensure that the impact on housing supply during the current crisis can be minimised. Direct stimulus (e.g. through VAT reduction) or measures such as shared equity schemes may be part of the solution. [1] https://blogs.imf.org/2020/04/14/the-great-lockdown-worst-economic-downturn-since-the-great-depression/ [2] Source: ESRI April 2020 [3] Source: Irish Times. 3rd April, 2020. “Housing market grinds to a halt as Covid-19 crisis takes hold”. [4] This is the Total Addressable Market – the number of potential purchasers will be lower of course.

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

About Us

Keogh Consulting looks to help individuals and organisations deliver the right projects the right way. Here is some of our knowledge and a few case studies that we hope will help you on your project journey.

Categories

All

Project Cost Calculator & Database

Cost Rental Simple Model

Cost Rental Complex Model

|

RSS Feed

RSS Feed

Service |

Company

|

|