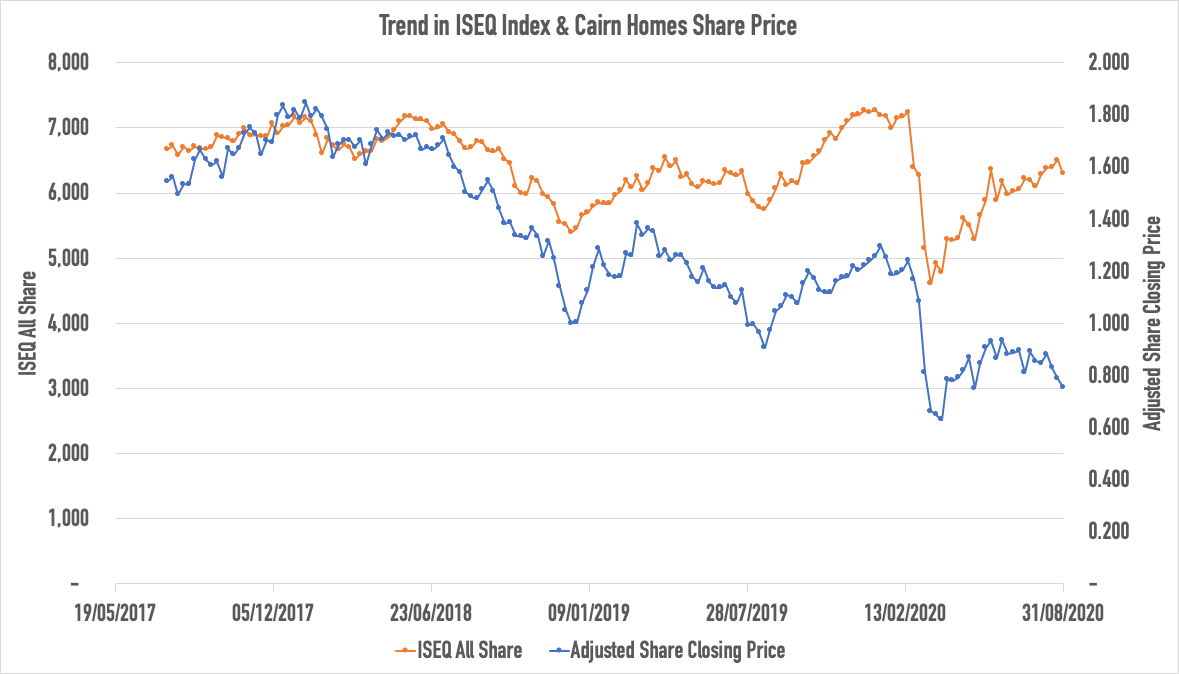

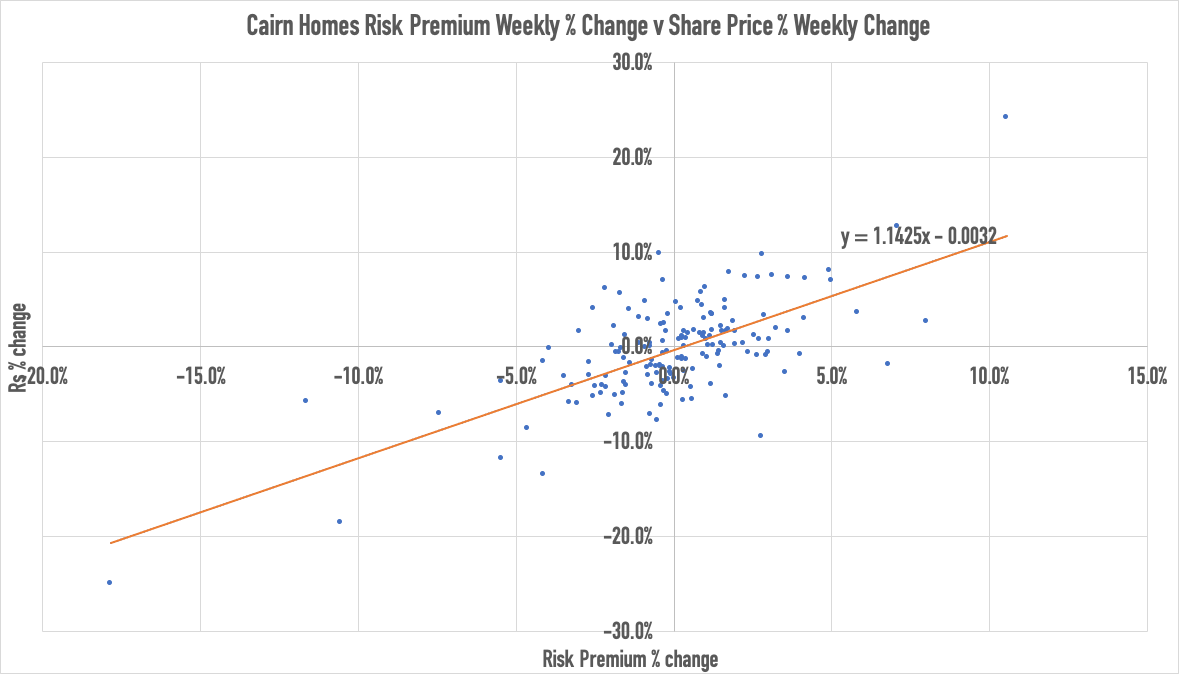

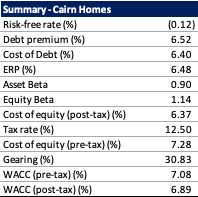

Trend in Cairn Homes Share Price v ISEQ Index Introduction A residential property projects revenues must exceed costs for a project to be viable. Included in these costs are the cost of funding the project, usually a mix of debt and equity. The cost of debt is clear and comes from the interest charge on debt (either on a project specific or company basis), however, how is the cost of equity capital (i.e. the minimum expected return required by an equity investor from their investment) estimated? For a residential property project the required return over the investment period is based on its risk when compared with returns earned on competing investments and other capital market benchmarks. This article (download here) looks at how to estimate the cost of equity for a residential project. Cost of Equity The standard formula for estimating a company’s cost of equity, Re, or, depending on your perspective, an investor’s required rate of return on equity – is the capital asset pricing model (“CAPM”). The formula, which has remained fundamentally unchanged for almost four decades, states that a company’s cost of equity is equal to the risk-free rate of return, Rf, plus a premium to reflect the extra risk of the investment in question. For a project, as opposed to a company, the CAPM formula can be used when the assumption is made that the risk free return and the excess market return will remain approximately constant over the life of the project – for a two to three year project this is usually appropriate. The CAPM formula is: Re = Rf + Beta x (TMR – Rf), where, Rf = is the risk-free rate; Beta = the sensitivity of a company’s equity returns to the market TMR = expected return of the market (TMR – Rf) = market risk premium A brief explanation and summary of assumptions around the three elements of the formula are outlined below: Risk Free Rate, Rf While nothing is completely risk-free, the rate of return of a long term government rate denominated in the same currency as cash flow from the project is generally used as the risk-free rate (i.e in this case a 10- Year Irish Government Bond), Rf, because of the low volatility of this type of investment and the fact that the return is backed by the government. This is calculated by the yield on a 10 year bond from market data. On date of this calculation (4th September) the yield on 10 Year Irish Government Bonds was -0.12% Beta What does Beta mean? A company’s Beta is a reflection of its volatility relative to the wider market. A Beta of 1 indicates the stock moves in sync with the broader market, while a Beta above 1 indicates greater volatility than the market. Conversely, a Beta lower than 1 indicates the stock's valuation is more stable. The approach to take is to use the Beta value of the industry within which the project could be classified as a surrogate for the Beta value of the project. Market data for the industry, in this case quoted housing companies (e.g. Glenveagh PLC, Cairn Homes PLC) or residential rental companies (e.g. IRES REIT) is used as a proxy for residential development or residential rental industries. The quoted companies Beta (Betaequity) is calculated from market data and then unleveraged to give an industry Beta (Betaasset). The method to do so is outlined below. Market Risk Premium, TMR - Rf The market risk premium, (TMR – Rf), is the difference between the expected return on a market portfolio and the risk-free rate. The market risk premium is difficult to measure and is most commonly obtained from published data such as the “Credit Suisse Global Investment Returns Yearbook” or from calculations made by experts such as Aswath Damodaran: http://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/ctryprem.html In July 2020 the market risk premium for Ireland was estimated at 6.48% by Damodaran. Calculating Beta: It may seem redundant to calculate Beta, since it's a widely used and publicly available metric (e.g. on Yahoo Finance) but there's one reason to do it manually: the fact that different sources use different time periods in calculating returns. While Beta always involves the measurement of variance and covariance over a period, there is no universal, agreed-upon length of that period. Therefore, one analyst may use five years of monthly data (60 periods over five years), while another may use one year of weekly data (52 periods over one year) in coming up with a Beta number. The resultant differences in Beta may not be huge, but consistency can be crucial in making comparisons. The most common regression used to estimate a company’s raw Beta is the market model: Ri = alpha + Beta x Rm + e, where: The stocks return, Ri, is regressed against the market’s return, Rm  Calculation of Cairn Homes Beta Using excel the method to calculate Beta is as follows:

Summary

The minimum expected return required by an equity investor from their investment in Cairn Homes is 7.28% on a pre-tax basis (residential property development company asset beta 0.90). This is compared to 3.75% for an investor in IRES REIT (residential build to rent company asset beta 0.30). These asset Betas can be used as a proxy for the Beta of a project in either of the 2 sectors with an appropriate adjustment. For a residential project financed with 60% debt & 40% equity : Beta equity = Beta asset x (1 + D/E) Beta equity = 0.90 x (1 + 60/40) = 2.25, and Re = Rf + Beta x (TMR – Rf), where, Re = -0.12% + 2.25 x 6.48% = 14.46% Thus, with this funding structure the minimum expected return by an equity investor for their investment in a residential development project is 14.46%

0 Comments

Your comment will be posted after it is approved.

Leave a Reply. |

About Us

Keogh Consulting looks to help individuals and organisations deliver the right projects the right way. Here is some of our knowledge and a few case studies that we hope will help you on your project journey.

Categories

All

Project Cost Calculator & Database

Cost Rental Simple Model

Cost Rental Complex Model

|

RSS Feed

RSS Feed

Service |

Company

|

|